@tlas Insights

- Cheap Words

- Commission Plans

- Comp Plans

- Contract Tips

- Convertible Notes

- Dilution is your friend

- Finplan Vs. Budget

- Focus Kills Companies

- Freemium Vs. Premium

- Funding Process

- Let's Change Topics

- Sales Pipeline

- Sales Expectations

- Significant Digits

- ST Goals

- The Nerd's Prayer

- To Better Days

- Top Ten Failures

- VC Tips

- Your Pitch

Finplan Vs. Budget

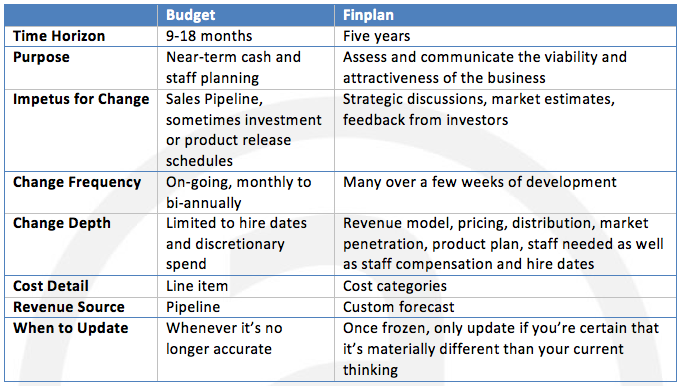

Do I need to tell you about the importance of financial planning? Sheeesh, I hope not. Without a reasonable outlook, you don’t know how much money to raise now or when to start working on the next round or when to begin recruiting for needed positions.Time Horizon

There are two time horizons of financial planning and a tool for each. The near term is this year. We define this loosely. If we’re more than, say, six months into the year, then we’ll look up to 18 months in the future to the end of the next calendar year; otherwise, we consider the current calendar year. The extended term is five years – the range for which most investors expect you to project pro-forma results. To manage near term operations, we develop a budget. Finplans suit the extended term. But why the difference and why can’t I just have one document? Well, you could and we’ve tried.

Purposes of Budgets and Finplans

Budgets answer these questions:

- Will I be able to make payroll next month?

- How much more do I need to raise to keep the company going though our beta release in six months?

- Should I be recruiting for any new positions now in order to have staff on board the plan calls for them?

- Is it prudent to put this $100k over-subscription of our round into marketing?

- Do I need to adjust some discretionary spend in the coming months due to recent performance (considered at a department level in more advanced companies)?

Level of Detail

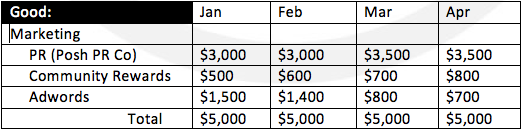

Budgets must be prepared at a line-item level, using the company’s chart of accounts. This is needed for budget v actual reports. We issue these to develop “responsibility accounting” whereby department heads can become responsible for their group. These reports are required if a CEO is going to delegate any budget responsibility or spend authority. Line item level of detail is needed to plan exact costs such as rent, which grows (or shrinks) as a step function. The budget will show us exactly when the company plans to move and by how much rent will increase at that time. Your budget should facilitate easy changes to hire dates and discretionary spending. It should clearly identify what you’re planning on buying. The above budget detail forces the user to think tactically about his marketing plan. This pays off when it comes time for execution. Also, if adjustments are needed, the user will think about cuts at meaningful level, not just arbitrary reductions or additions.

The above budget detail forces the user to think tactically about his marketing plan. This pays off when it comes time for execution. Also, if adjustments are needed, the user will think about cuts at meaningful level, not just arbitrary reductions or additions.

Change, nothin’ stays the same

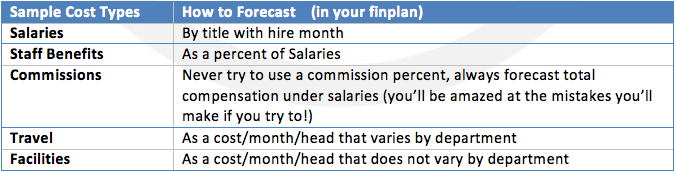

(Van Halen) The frequency and nature of updates is a key driver for the development of these parallel financial tools. Finplans support events (typically fundraising) while budgets support on-going operations. The life of a finplan is measured in weeks, after which it’s shelved to be updated for the next event. These are intense weeks likely to result in radical changes in company fundamentals, from selling a product to selling a service or releasing a consumer version or all matter of fundamental alterations to the company’s core business. A robust finplan will deal with these and provide a P&L;, Balance Sheet and Statement of Cash Flows (bonus points if they reconcile to one another!) with relative ease. While you’re debating the merits and examining the impact of creating a professional version of your turnip dicer to sell to restaurant supply houses, you need to be able to focus on these changes without the distraction of cost details. So, your finplan should not be built with a charts of accounts. Instead, it should use broad cost categories like Equipment, Travel, and Facilities. These cost categories should be populated with formulas rather than amounts – formulas like $800 per head for facilities and $2k per sales head for travel. Formulas such as these allow for a single input that scales (more or less) as you consider different strategies. Of course, staffing must be forecasted at far deeper level of detail and, if your business is capital intense, then that too. By ignoring step-functions or other detailed cost-drivers for minor costs, these formulas ensure that costs are approximately correct on an annual basis while avoiding the potential that they may have been forescast completely wrong (because committing to more detail inevitably results in user error) and they result in a tool that fully meets the objectives of a finplan.

Using formula-driven costs for most of your categories allows you to focus on the strategic changes that matter.

By ignoring step-functions or other detailed cost-drivers for minor costs, these formulas ensure that costs are approximately correct on an annual basis while avoiding the potential that they may have been forescast completely wrong (because committing to more detail inevitably results in user error) and they result in a tool that fully meets the objectives of a finplan.

Using formula-driven costs for most of your categories allows you to focus on the strategic changes that matter.